About Us

Executive Editor:Publishing house "Academy of Natural History"

Editorial Board:

Asgarov S. (Azerbaijan), Alakbarov M. (Azerbaijan), Aliev Z. (Azerbaijan), Babayev N. (Uzbekistan), Chiladze G. (Georgia), Datskovsky I. (Israel), Garbuz I. (Moldova), Gleizer S. (Germany), Ershina A. (Kazakhstan), Kobzev D. (Switzerland), Kohl O. (Germany), Ktshanyan M. (Armenia), Lande D. (Ukraine), Ledvanov M. (Russia), Makats V. (Ukraine), Miletic L. (Serbia), Moskovkin V. (Ukraine), Murzagaliyeva A. (Kazakhstan), Novikov A. (Ukraine), Rahimov R. (Uzbekistan), Romanchuk A. (Ukraine), Shamshiev B. (Kyrgyzstan), Usheva M. (Bulgaria), Vasileva M. (Bulgar).

Economics

PDF

PDFIntroduction. An important stage of Russian innovative system formation and enhance the innovation activities is the creation and development of innovation infrastructure. Various innovation infrastructure elements solve different problems, in particular, promotion the effective development and implementation of innovative projects and provision of Advisory services.

The major problems associated with: high cost knowledge-intensive activities; the absence of effective mechanism to reduce costs; the inadequacy monitoring costs in the design, manufacture and promotion of high-tech products and technologys for timely management decisions; the lack of qualified specialists in the cost management field.

In this regard, the problem of optimal cost control is most important due to the close connection between the expenditure and revenues. In this article to implement the idea of monitoring at all stages of the innovation process offers the method contour of the limiting allowable costs.

Goal. Improving the efficiency of cost management infrastructure elements of the innovation system on the stages of design, production and promotion of innovative products and technologies.

By synthesizing national and international experience in the cost management, and the critical analysis of theory and practice of implementation of this process the authors were able to formulate a set of methods that can be successfully used in the decision-making both in strategic and tactical planning effort to develop the planned and actual costs [1, 2, 3, 4, 5, 6, 7, 8]:

Authors have developed the conceptual diagram of the cost management, which gives a general idea of the mechanism of expenditure formulation, the relationship of the cost components and the effect of the mechanisms of the cost management [9].

The modelling of such a contour requires the selection of the most important indicators, which characterize the level of costs; the establishment of interfaces and interdependencies between these factors; the determination of the most likely trend of changing parameters; the rate of change in different situations, etc

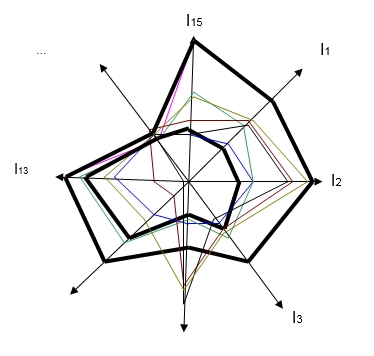

The change in each cost element and the indicator of organization activity can be represented as a vector, whose angle to the axes defined by the rate of change indicators. This angle is given, as a kind of norm. (see Figure 1)

Symbols:

I – indicators:

I1 – raw materials;

I2 – hardware;

………;

I13 – total cost;

I15 – output.

Figure 1. The contour of the limiting allowable costs

Conclusion. Contour allows the implementation of operational control over the fixed and variable costs of the organization, identification of the potential to reduce the total cost or its individual components; determination of the optimal cost to deliver the best possible outcome; determination of the threshold of profitability (sales), the lower and upper boundaries of cost-drivers; cost management in any given point in time.

2. Horngren C.T., Foster G. Cost Accounting: A Managerial Emphasis. Hall Inc. USA. 1987.

3. Margarida Sanz, J.C. La Gestion de Costes Basada en las Actividades (ABC/ABM). Implantacion en centros asistenciales de personas con retraso mental. Valladolid: Universidad de Valladolid, 2003.

4. Moscove S., Crowningshield G., Gorman K. Cost Accounting with managerial Applications. Houghton Miffin Company. USA. 1985.

5. Oriol, A., Soldevila, P. Contabilidad y Gestion de Costes – 5a edicion – Barcelona: Profit, 2010.

6. Reading in managerial economics. Ed. by I.B.Ibrahim /a.o./ Oxford /a.o./1976.

7. Seicht G. Moderne Kosten- und Leistungsrechnung. Grundlagen und praktische Gestaltung. – Industrieverlag Peter Linde, GmbH. – Wien. 1990.

8. Target Costing. Munchen: Herausgeber Controller Verein eV, 1997.

9. Yurchenco T., Vorontsova Y. Cost management in the organization / State University of Management – Moscow, 2016.

Zelentsova L., Vorontsova Y. MECHANISM COST MANAGEMENT INFRASTRUCTURE ELEMENTS OF THE INNOVATION SYSTEM. International Journal Of Applied And Fundamental Research. – 2016. – № 2 –

URL: www.science-sd.com/464-25180 (25.06.2026).